International (EN)

International (EN) India (EN)

India (EN)

The pandemic related lockdown and various restrictions imposed in India has severely impacted businesses and the economy overall. With zero to minimal capacity utilisation and negligible sales from the period of April’20 to Aug’20, the credit quality of Indian corporates declined substantially. This led to a double blow where in the credit quality of the borrowers reduced substantially and it also led to lay-offs and increased unemployment.

This impacted the already ailing Indian financial sector all the more due to reduction in credit deployment and increasing NPLs. However, the disruptions were limited in lieu of the measures taken by RBI in providing moratorium and the government support to provide requisite working capital and special loans.

Credit Deployment

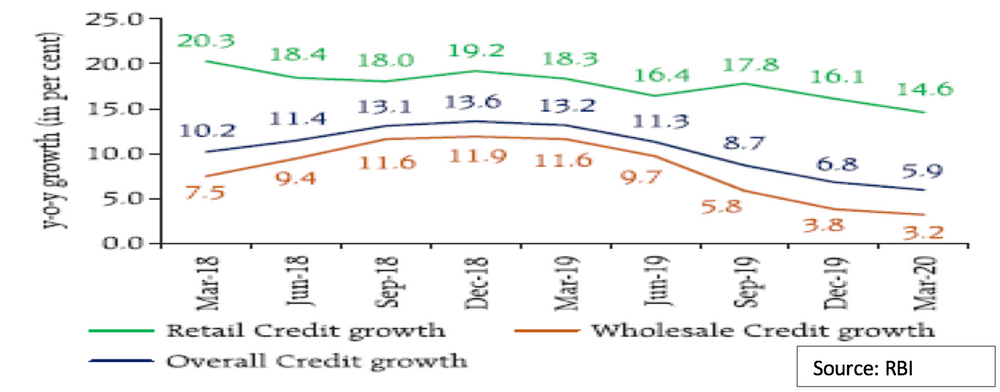

The overall credit growth of banks had been slowing from Mar’18-Mar’20 owing to slowdown in growth of wholesale lending. However, as can be seen from the chart below, the retail loans were contributing the maximum growth in the last 3 years as compared to wholesale credit.

The gross bank credit of Indian Banks declined by 1.7% in between March’20 to Aug’20. This was the same period when maximum restrictions were imposed due to Covid-19. Retail loans which include consumer durable, housing, education, vehicle, credit card loans and other personal loans constitute 25%-30% of the total banking portfolio declined by 0.2% in the period March’20-Aug’20 for the first time in the last three years.

Initiatives from the Regulators and Government

In order to mitigate the burden of debt servicing and enable the continuity of viable businesses and households, Reserve bank of India (RBI) announced a number of regulatory and supervisory measures. These included policy initiatives like easing of monetary policies, liquidity measures like Targeted long-term repo operations, CRR and repo rate cuts etc.

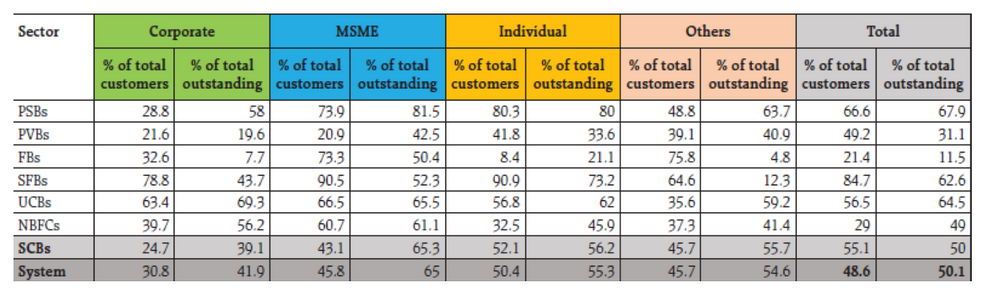

Other than this, RBI had allowed re-schedulement of payments, interests, monthly instalments, moratorium from three months to two years. Understanding that retail borrowers could also face challenges and pressures owing to salary cuts and job losses, the RBI allowed moratorium as well as restructuring of retail loans. RBI also permitted the banks to continue maintaining the classification of these assets as standard. This moratorium was availed by almost 50% of households under the category of retail loans (Source: RBI)

Impact on NPLs

The restructuring and moratorium allowed by the RBI helped the banks in maintaining their asset quality. As per a Crisil Research report, had it not been allowed, non-performing assets would have touched a two-decade high of 11.5% by the end of this year.

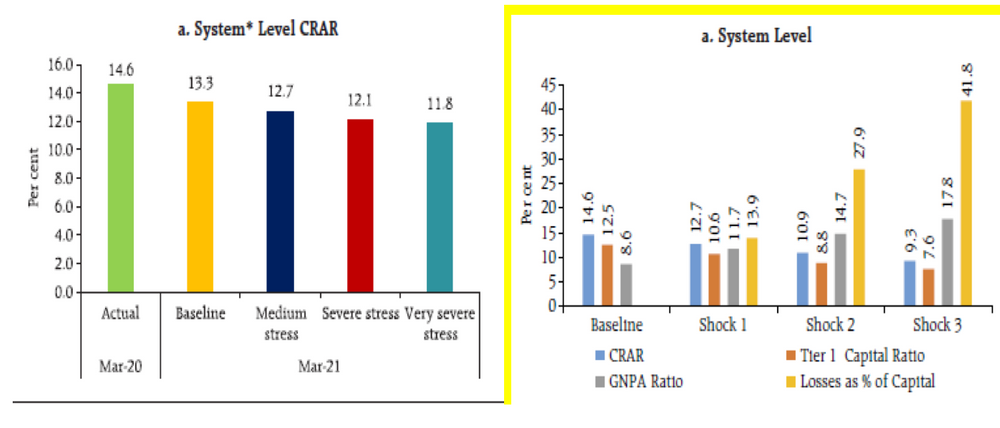

As per the report released in July’2020, Reserve Bank of India (RBI) conducted a stress test on the Gross Non-performing Assets (GNPA) ratio of the banks. The stress tests indicated that the GNPA ratio of all banks may increase from 8.5% in March 2020 to 12.5% by March 2021 under the baseline scenario. If the macroeconomic environment worsens further, the ratio may escalate to 14.7% under the very severely stressed scenario. This is likely to lead to fall in Capital Adequacy Ratio from 14.6% in Mar’20 to 13.3% or 11.8% in Mar’21 under the baseline or very severe stress scenario respectively.

Given this fear of increased asset stress in banking industry, the Government of India (GOI) also on its part, worked out a support package entailing a prudent mix of sovereign guarantee based schemes, direct fiscal expenditure and longer-term structural policy reforms. For the time being these support measures have alleviated the financial industry risk at least for now.

What has Changed for the Banks During and Beyond COVID?

While RBI and GOI have supported the economy with stimulus packages, liquidity windows, deferment of NPAs, the overall banking industry tried undergoing a major overhaul. The various challenges in-front of the banking industry included:

- Decline in revenue generation due to lower customer footfalls, lower demand, reduced and remote working of staff.

- Likely stress on net interest income owing to skewed interest expense.

- Requirement of additional provisioning owing to an increase in expected stressed assets.

All banks reengineered and redrafted their business continuity plans. Banks tried shifting towards asset light models with higher focus on digital transactions and remote working. Lending, which was earlier a mix of physical and digital processes has completely moved to digital platforms. Banks’ mode of interaction with customers has also changed to online modes rather than physical modes. Banking operations in India which were earlier primarily centred around bank branches due to the large volumes of cash transactions shifted to digital platforms and interactions.

Policies, payments and collections, cash management, Information Technology, market analytics, customer understanding, risk analytics which had earlier being backend functions for banks, became their core functions. Banks became more agile in making these functions digitally and technologically oriented.

The impact of Moratorium on Borrowers’ Behaviour

It is important to note that borrowers’ payment behaviour underwent a drastic change. As borrowers started realising limitations towards visiting branches, customers adapted to digital channels and technology platforms for regular transactions, repayments and payments.

Going forward, overall borrowing is expected to decline with reduction in discretionary spending. In the wake of economic distress triggered by the coronavirus pandemic, most people will prefer small ticket sized loans for emergencies or for financing immediate requirements. At the same time, with growing concerns for increase in NPAs, banks are also expected to tighten their lending norms and only those customers with strong credit background will be preferred.

In terms of loan repayments, borrowers availed the benefits of moratorium and used it to defer their repayments and EMIs. The recent loan moratorium announced by the RBI to extend economic reprieve to struggling borrowers has been mistaken for complete loan waivers. In the event of non-receipt of interest from borrowers, banks will also struggle to pay their customers interests on their deposits. Thus, the banking industry as a whole will need to ensure an improvement in loan repayment behaviour. Even RBI has made it clear that it should not be considered as a regular feature. The same is only allowed for borrowers and sectors deeply impacted by Covid-19 related slow-down and should not be considered a broad-brush approach.

Conclusion

With restrictions and social distancing norms still in place, banking operations as well as consumer behaviour both are expected to change further in the future. Banks have to rethink and rework their strategy in order to be more effective and customer friendly. Banks will have to continue encouraging and educating their customers to migrate to digital channels especially in Tier-II and Tier-III cities in India. Banks need to build modern digital technologies and advanced analytics to have sustainable competitive advantage.